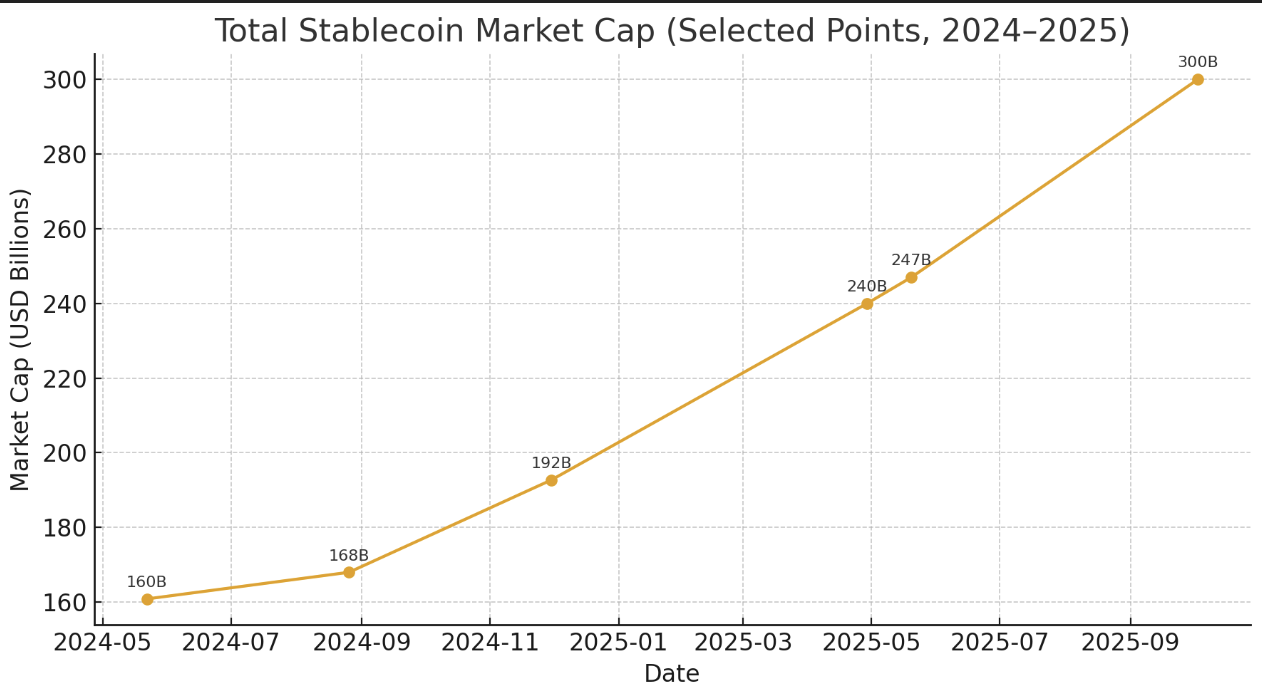

Internet native payment infrastructure is scaling faster than anticipated. Stablecoins have reached $280B and are projected to reach $2-4T by 2030. Neobanks like Plasma and Tempo are positioned to absorb liquidity from traditional banks. AI agents are leveraging crypto rails for micropayments (e.g., via x402), emerging as a new payment class. Traditional finance, including forex markets ($9.6T daily volume), is testing on-chain settlement.

The good news is, money is moving on-chain at unprecedented scale and speed.

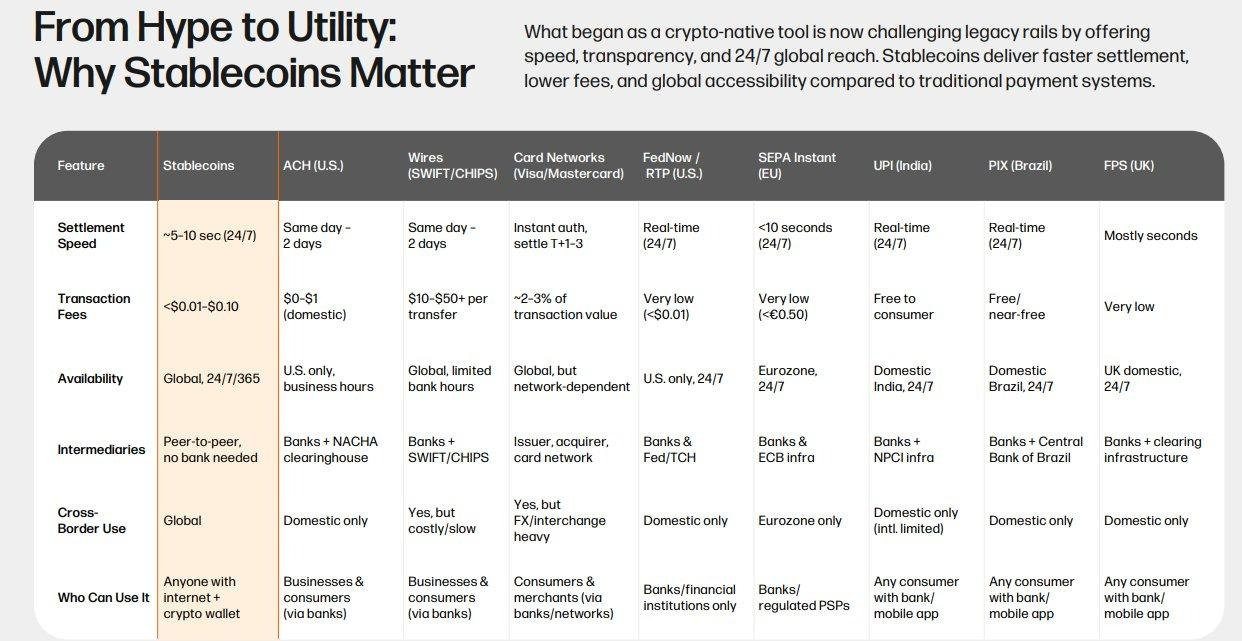

But this growth creates a critical constraint: efficiency at scale. As trillions of dollars move on-chain, the infrastructure built for an earlier era – low transaction volume, high margins – can’t keep up. Existing solutions create bottlenecks as chains multiply, with point-to-point bridges scaling as N²: each chain must connect to every other individually, exponentially increasing complexity. Moving money for tens of cents or dollars and taking weeks to months to open new corridors simply isn’t good enough.

Polymer is the payment verification network that solves this.

Through novel proof-based verification, Polymer removes friction and unifies fragmented networks into a reliable payment layer for the on-chain economy. With intent verification instead of point-to-point bridges, a single API integration, and a unified verification standard across all chains, Polymer delivers a fundamentally different cost structure and operational model: payments move for 1 cent or less, and new chains launch within minutes instead of months.

As new integrations and product launches go live in Q4, Polymer is positioned to become the canonical payment verifier for a majority of intent-based crosschain payment volume. In a market where bridge spreads compress to basis points, the verifier with the best cost structure and fastest execution wins orderflow. We’re the infrastructure that doesn’t break under volume.

The market timing is compressed. Catalysts are moving simultaneously:

- Institutional stablecoin adoption: Stripe, Circle, major payment processors are moving billions on-chain. Plasma, Tempo, and others are building native neobank infrastructure on stablecoins.

- RWA protocols: Tokenized securities and real-world asset bridges are adding velocity to crosschain settlement. This is where institutional capital moves next.

- AI agents: Discovery, reputation, and payment settlement all require frictionless, trustless infrastructure. This is a new application class with exponential growth potential, something that the industry is witnessing in real-time with x402’s explosive growth.

The projected interoperability market: $1.5T+ in crosschain volume by the end of 2026.

The protocol that establishes network effects now will own this market for years. Applications built on Polymer become sticky; developers choose the fastest, cheapest verifier; and users benefit from better payment rails. Everyone wins from switching costs and network depth. This is a land-grab moment.

In a market growing this fast, the winner is whoever captures the most users first. The applications that build on Polymer now become advocates, and their users become Polymer’s users. Volume compounds.

Our north star is to solve the payment crisis head-on by building the infrastructure that makes on-chain money movement faster, cheaper, and more reliable than anything traditional finance can offer.

The best developer experience, the easiest integration process, the cheapest and the fastest infrastructure. That’s how Polymer wins. The future of finance runs on on-chain rails. 100x faster and 10x cheaper than the next closest competitor, Polymer is the verification layer that makes those rails viable at scale – positioned to capture this market at exactly the moment it becomes inevitable.

Polymer Powers Modern Money.